(2) Any amount already included in CET 1 Capital or Additional Tier 1 Capital must not be included in Tier 2 Capital.

(3) The amount to be included in the consolidated Tier 2 Capital of an Islamic Bank is calculated in accordance with the following formula:

NCI – ((T2s – Min) × SS)

where:

NCI is the total of the non-controlling interests of third parties in a consolidated Subsidiary of an Islamic Bank.

T2s is the amount of Tier 2 Capital of the subsidiary.

Min is the lower of:

(a) 10.5 %× (minimum Tier 2 Capital requirement of the subsidiary); and

(b) 10.5 % × (the part of the consolidated minimum Tier 2 Capital requirement that relates to the subsidiary).

SS means the percentage of the shares in the Subsidiary (being shares included in Tier 2 Capital) held by those third parties.

4.26. Treatment of third party interests from SPVs

(1) An instrument issued out of an SPV and held by a third party must not be included in an Islamic Bank’s CET 1 Capital. Such an instrument may be included in an Islamic Bank’s Additional Tier 1 or Tier 2 Capital (and treated as if it had been issued by an Islamic Bank itself directly to the third party) if:

(a) the instrument satisfies the criteria for inclusion in the relevant category of Regulatory Capital; and

(b) the only asset of the SPV is its investment in the capital of an Islamic Bank and that investment satisfies the criterion in rule 4.16 or 4.18 for the immediate availability of the proceeds.

(2) An instrument described in part (1) of this Rule that is issued out of a SPV through a consolidated Subsidiary of an Islamic Bank may be included in an Islamic Bank’s consolidated Additional Tier 1 or Tier 2 Capital if the instrument satisfies the criteria in rule 4.16 or 4.18, as the case requires. Such an instrument is treated as if it had been issued by the Subsidiary itself directly to the third party.

4.27. Regulatory adjustments

(1) Regulatory adjustments to an Islamic bank’s capital may be required to avoid double-counting, or artificial inflation, of its capital. They may also be required in relation to assets that cannot readily be converted into cash.

(2) Adjustments can be made to all 3 categories of Regulatory Capital, but most of them are to CET 1 Capital.

4.28. Approaches to valuation and adjustment

(1) An Islamic Bank must use the same approach for valuing regulatory adjustments to its capital as it does for balance-sheet valuations. An item that is deducted from capital must be valued in the same way as it would be for inclusion in an Islamic Bank’s balance sheet.

(2) An Islamic Bank must use the corresponding deduction approach and the threshold deduction rule in making adjustments to its capital.

4.29. Definitions

Entity concerned means:

(a) a financial entity (including an Islamic Bank and a takaful entity); or

(b) any other entity over which, under the relevant accounting standards, an Islamic Bank can exercise control.

Significant investment, by an Islamic Bank in an entity concerned, means an investment of 10% or more in the common shares, or other instruments that qualify as capital, of the entity concerned. Investment includes a direct, indirect and synthetic holding of capital instruments.

Guidance

(1) The notion of exercising control in this chapter is different from that in the definition of exercise control in the glossary. The term as defined in the glossary is used in relation to related parties and connected parties as they relate to Credit Risk, concentration risk and large exposures.

(2) The relevant accounting standards referred to (primarily AAOIFI and IFRS) use control in a much broader sense, so that an investor should consider all relevant facts and circumstances in assessing whether it controls an investee.

(3) Under IFRS 10, for example, an investor controls an investee if the investor has all of the following:

(і) power over the investee (that is, the investor has existing rights that give it the ability to direct the activities that significantly affect the investee’s returns)

(ii) exposure, or rights, to variable returns from its involvement with the investee

(iii) ability to use its power over the investee to affect the amount of the investor’s returns.

(4) Another example would be control through agreement with the entity’s other shareholders or with the entity itself. The agreement could result in control even if the investor holds less than majority voting rights, so long as those rights are substantive (that is, exercisable by the investor who has the practical ability to exercise them when relevant decisions are required to be made).

4.30. Adjustments to Common Equity Tier 1 Capital

Adjustments to CET 1 Capital must be made in accordance with the Rules specified in the following Rules 4.31 to 4.45. Regulatory adjustments are generally in the form of deductions, but they may also be in the form of recognition or de-recognition of items in the calculation of an Islamic Bank’s capital.

4.31. Goodwill and intangible assets

An Islamic Bank must deduct from CET 1 Capital the amount of its goodwill and other intangible assets (except real estate financing servicing rights). The amount must be net of any related deferred tax liability that would be extinguished if the goodwill or assets become impaired or derecognised under the relevant accounting standards.

4.32. Deferred tax assets

(1) An Islamic Bank must deduct from CET 1 Capital the amount of deferred tax assets (except those that relate to temporary differences) that depend on the future profitability of an Islamic Bank.

(2) A deferred tax asset may be netted with a deferred tax liability only if the asset and liability relate to taxes levied by the same taxation authority and offsetting is explicitly permitted by that authority. A deferred tax liability must not be used for netting if it has already been netted against a deduction of goodwill, other intangible assets or defined benefit pension assets.

Guidance

Any deferred tax liability that may be netted must be allocated pro rata between deferred tax assets under this rule and those under the threshold deduction rule. For the treatment of deferred tax assets that relate to temporary differences (for example, allowance for financing losses).

4.33. Cash flow hedge reserve

In the calculation of CET 1 Capital, an Islamic Bank must derecognise the amount of the cash flow hedge reserve that relates to the hedging of items that are not fair-valued on the balance sheet (including projected cash flows).

4.34. Cumulative gains and losses from changes to own Credit Risk

In the calculation of CET 1 Capital, an Islamic Bank must derecognise all unrealised gains and unrealised losses that have resulted from changes in the fair value of liabilities that are due to changes in an Islamic Bank’s own Credit Risk.

4.35. Defined benefit pension fund assets

(1) An Islamic Bank must deduct from CET 1 Capital the amount of a defined benefit pension fund that is an asset on an Islamic Bank’s balance sheet. The amount must be net of any related deferred tax liability that would be extinguished if the asset becomes impaired or derecognised under the relevant accounting standards.

(2) An Islamic Bank may apply to the AFSA for approval to offset from the deduction any asset in the defined benefit pension fund to which an Islamic Bank has unrestricted and unfettered access. Such an asset must be assigned the risk-weight that would be assigned if it were owned directly by an Islamic Bank.

4.36. Securitisation gains on sale

In the calculation of CET 1 Capital, an Islamic Bank must derecognise any increase in Equity Capital or CET 1 Capital from a securitisation or re-securitisation transaction (for example, an increase associated with expected future margin income resulting in a gain-on-sale).

4.37. Assets lodged or pledged to secure liabilities

(1) An Islamic Bank must deduct from CET 1 Capital the amount of any assets lodged or pledged by it, if:

(a) the assets were lodged or pledged to secure liabilities incurred by the Islamic Bank; and

(b) the assets are not available to meet the liabilities of the Islamic Bank.

(2) The AFSA may determine that, in the circumstances, the amount of assets lodged or pledged need not be deducted from an Islamic Bank’s CET 1 Capital.

4.38. Acknowledgments of debt

(1) An Islamic Bank must deduct from CET 1 Capital the net present value of an acknowledgement of debt outstanding issued by it to directly or indirectly fund instruments that qualify as CET 1 Capital.

(2) This rule does not apply if the acknowledgement is subordinated in rank similar to that of instruments that qualify as CET 1 Capital.

4.39. Accumulated losses

An Islamic Bank must deduct from its CET 1 Capital the amount of any accumulated losses.

4.40. Deductions from categories of Regulatory Capital

(1) The deductions that must be made from CET 1 Capital, Additional Tier 1 Capital or Tier 2 Capital under the corresponding deduction approach are set out in this section of IBB Module. An Islamic Bank must examine its holdings of index securities and any underlying holdings of capital to determine whether any deductions are required as a result of such indirect holdings.

(2) Deductions must be made from the same category for which the capital would qualify if it were issued by the Islamic Bank itself or, if there is not enough capital at that category, from the next higher category.

(3) The corresponding deduction approach applies regardless of whether the positions or exposures are held in the Banking Book or Trading Book.

(4) If the amount of Tier 2 Capital is insufficient to cover the amount of deductions from that category, the shortfall must be deducted from additional Tier 1 Capital and, if additional Tier 1 Capital is still insufficient, the remaining amount must be deducted from CET 1 Capital.

4.41. Investments in own shares and Capital instruments

(1) An Islamic Bank must deduct direct or indirect investments in its own common shares or own capital instruments (except those that have been derecognised under the relevant accounting standards). The Islamic Bank must also deduct any of its own common shares or instruments that it is contractually obliged to purchase.

(2) The gross long positions may be deducted net of short positions in the same underlying exposure only if the short positions involve no counterparty risk. However, gross long positions in its own shares resulting from holdings of index securities may be netted against short positions in its own shares resulting from short positions in the same underlying index, even if those short positions involve counterparty risk.

4.42. Reciprocal cross holdings

An Islamic Bank must deduct reciprocal cross holdings in shares, or other instruments that qualify as capital, of an entity concerned.

4.43. Non-significant investments—aggregate is less than 10% of firm’s Common Equity Tier 1 Capital

(1) This rule applies if:

(a) an Islamic Bank makes a non-significant investment in an entity concerned;

(b) the entity concerned is an unconsolidated entity (that is, the entity is not included in an Islamic Bank’s consolidated returns);

(c) an Islamic Bank does not own 10% or more of the common shares of the entity concerned; and

(d) after applying all other regulatory adjustments, the total of the deductions required to be made under this rule is less than 10% of an Islamic Bank’s CET 1 Capital.

(2) An Islamic Bank must deduct any investments in common shares, or other instruments that qualify as capital, of an entity concerned.

(3) The amount to be deducted is the net long position (that is, the gross long position net of short positions in the same underlying exposure if the maturity of the short position either matches the maturity of the long position or has a residual maturity of at least 1 year).

(4) Underwriting positions held for more than 5 business days must also be deducted.

(5) If a capital instrument is required to be deducted and it is not possible to determine whether it should be deducted from CET 1 Capital, Additional Tier 1 Capital or Tier 2 Capital, the deduction must be made from CET 1 Capital.

4.44. Non-significant investments—aggregate is 10% or more of firm’s Common Equity Tier 1 Capital

(1) This rule applies if, after applying all other regulatory adjustments, the total of the deductions required to be made under rule 4.43 is 10% or more of an Islamic Bank’s CET 1 Capital.

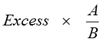

(2) An Islamic Bank must deduct the amount by which the total of the deductions required to be made under rule 4.43 exceeds 10% of an Islamic Bank’s CET 1 Capital. This amount to be deducted is referred to as the excess.

(3) The excess to be deducted from each category of Regulatory Capital under the corresponding deduction approach is calculated in accordance with the following formula:

where:

A is the amount of CET 1 Capital, additional Tier 1 Capital or Tier 2 Capital of the Islamic bank, as the case requires.

B is the total capital holdings of the Islamic Bank.

4.45. Significant investments

(1) This rule applies if:

(a) an Islamic Bank makes a significant investment in an entity concerned;

(b) the entity concerned is an unconsolidated entity (that is, the entity is not included in an Islamic Bank’s consolidated returns); and

(c) an Islamic Bank owns 10% or more of the common shares of the entity concerned.

(2) An Islamic Bank must deduct the total amount of investments in the entity concerned (other than investments in common shares, or other instruments that qualify as CET 1 Capital, of the entity).

(3) For the treatment of investments in common shares, or other instruments that qualify as CET 1 Capital, of an entity concerned, see Rule 4.46 (Deductions from Common Equity Tier 1 Capital).

(4) The amount to be deducted is the net long position (that is, the gross long position net of short positions in the same underlying exposure if the maturity of the short position either matches the maturity of the long position or has a residual maturity of at least 1 year).

(5) Underwriting positions held for more than 5 business days must also be deducted.

(6) If a capital instrument is required to be deducted and it is not possible to determine whether it should be deducted from CET 1 Capital, Additional Tier 1 Capital or Tier 2 Capital, the deduction must be made from CET 1 Capital.

4.46. Deductions from Common Equity Tier 1 Capital

(1) In addition to the other deductions to CET 1 Capital under this Chapter, deductions may be required to CET 1 Capital under the threshold deduction rule.

(2) The threshold deduction rule provides recognition for particular assets that are considered to have some limited capacity to absorb losses. The following items come within the threshold deduction rule:

(a) significant investments in the common shares, or other instruments that qualify as CET 1 Capital, of an unconsolidated entity concerned;

(b) real estate financing servicing rights;

(c) deferred tax assets that relate to temporary differences (for example, allowance for credit losses).

(3) Instead of full deduction, the items that come within the threshold deduction rule receive limited recognition when calculating CET 1 Capital. The total of each of the items in (2) above, do not require adjustment from CET 1 Capital and are risk-weighted at 300% (for items listed on a recognised exchange) or 400% (for items not so listed) provided that:

(a) each item is no more than 10% of an Islamic Bank’s CET 1 Capital (net of all regulatory adjustments except those under this section); or

(b) in total, the 3 items are no more than 15% of an Islamic Bank’s CET 1 Capital (net of all regulatory adjustments except those under this Subdivision).

(c) An Islamic Bank must deduct from CET 1 Capital any amount in excess of the threshold in (3) (a) or (b).

5. CAPITAL BUFFERS AND OTHER REQUIREMENTS

5.1. Introduction

(1) The Basel III capital adequacy framework contains 2 additional measures for conserving capital through the Capital Conservation Buffer and the Counter-Cyclical Capital Buffer.

(2) The Capital Conservation Buffer promotes the conservation of capital and the build-up of a buffer above the minimum in times of economic growth and credit expansion leading to profitability, so that the buffer can be drawn down in periods of stress. It imposes an obligation to restrict a firm’s distributions when capital falls below the Capital Conservation Buffer minimum.

(3) The rules requirements relating to application of Capital Conservation Buffer are set out in this Chapter.

5.2. Capital Conservation Buffer

(1) An Islamic Bank whose Risk-based Capital Requirement is higher than its Base Capital Requirement must maintain a minimum Capital Conservation Buffer of:

(a) 2.5% of its total RWA; or

(b) a higher amount that the AFSA may, by written notice, set from time to time.

(2) A firm’s Capital Conservation Buffer must be made up of CET 1 Capital above the amounts used to meet an Islamic Bank’s CET 1 Capital ratio, Tier 1 Capital ratio and Regulatory Capital ratio in rule 4.11).

(3) Capital raised through the issuance of sukuk cannot form part of the Capital Conservation Buffer because that capital does not qualify as CET 1 Capital.

5.3. Capital Conservation Ratio

(1) If an Islamic bank’s Capital Conservation Buffer falls below the required minimum, the Islamic Bank must immediately conserve its capital by restricting its distributions.

(2) This rule sets out, in column 3 of table 5.1, the minimum Capital Conservation Ratios for Islamic bank that are required to maintain a Capital Conservation Buffer. Capital Conservation ratio is the percentage of earnings that a firm must not distribute if its CET 1 Capital ratio falls within the corresponding ratio in column 2 of that table.

(3) Earnings means distributable profits calculated before deducting elements subject to the restrictions on distributions. Earnings must be calculated after notionally deducting the tax that would have been payable had none of the distributable items been paid.

(4) If the Islamic Bank is a member of a Financial Group, the Capital Conservation Buffer applies at group level.

(5) A payment made by a firm that does not reduce its CET 1 Capital is not a distribution for the purposes of this Chapter. Distributions include, for example, dividends, share buybacks and discretionary bonus payments.

(6) The effect of calculating earnings after tax is that the tax consequence of the distribution is reversed out.

(7) An Islamic Bank must have adequate systems and controls to ensure that the amount of distributable profits and maximum distributable amount are calculated accurately. An Islamic Bank must be able to demonstrate that accuracy if directed by the AFSA.

Guidance: Examples of application of table

Assume that a firm’s minimum CET 1 Capital ratio is 4.5% and an additional 2.5% Capital Conservation Buffer (which must be made up of CET 1 Capital) is required for a total of 7% CET 1 Capital ratio. Based on table 5.1:

(і) If a firm’s CET 1 Capital ratio is 4.5% or more but less than 5.125%, an Islamic Bank needs to conserve 100% of its earnings.

(ii) If a firm’s CET 1 Capital ratio is 5.125% or more but less than 5.75%, an Islamic Bank needs to conserve 80% of its earnings and must not distribute more than 20% of those earnings by way of dividends, share buybacks and discretionary bonus payments.

(iii) A firm with a CET 1 Capital ratio of more than 7% can distribute 100% of its earnings.

Table 5.1 Minimum Capital conservation ratios

| item | CET 1 Capital ratio | Minimum Capital conservation ratio (% of earnings) |

| 1 | 4.5% to 5.125% | 100 |

| 2 | ≥5.125% to 5.75% | 80 |

| 3 | ≥5.75% to 6.375% | 60 |

| 4 | ≥6.375% to 7.0% | 40 |

| 5 | ≥7% | 0 |

5.4. Powers of the AFSA

(1) The AFSA may impose a restriction on capital distributions by an Islamic Bank even if the amount of an Islamic Bank’s CET 1 Capital is greater than its CET 1 Capital ratio and required Capital Conservation Buffer.

(2) The AFSA may, by written notice, impose a limit on the period during which an Islamic Bank may operate within a specified Capital Conservation Ratio.

(3) An Islamic Bank may apply to the AFSA to make a distribution in excess of a limit imposed by this Chapter. The AFSA will grant approval only if it is satisfied that an Islamic Bank has appropriate measures to raise capital equal to, or greater than, the amount an Islamic Bank wishes to distribute above the limit.

5.5. Capital reductions

(1) An Islamic Bank must not reduce its capital and reserves without the AFSA’s written approval.

(2) An Islamic Bank planning a reduction must prepare a forecast (for at least 2 years) showing its projected capital after the reduction. The Islamic Bank must satisfy the AFSA that its capital will still comply with the IBB Module after the reduction.

Guidance: Examples of ways to reduce Capital

1) a share buyback or the redemption, repurchase or repayment of capital instruments issued by an Islamic Bank

2) trading in an Islamic Bank’s own shares or capital instruments outside an arrangement agreed with the AFSA.

3) a special dividend.

5.6. AFSA can require other matters

Despite anything in these rules, the AFSA may require an Islamic Bank to have capital resources, comply with any other capital requirement or use a different approach to, or method for, capital management. The AFSA may also require a firm to carry out stress-testing at any time.

5.7. Leverage Ratio

(1) The rule requirements relating to Leverage ratio specified in Rule 5.7 apply only to Islamic Banks excluding entities licensed to Providing Islamic Financing and Dealing in Investments as principal in a Shari’ah-compliant manner.

(2) An Islamic Bank must calculate its Leverage Ratio in accordance with the following formula:

Leverage ratio =

Where:

(a) «Capital measure» represents T1 Capital of the Islamic Bank calculated in accordance with Rule 4.12; and

(b) «Exposure measure» represents the value of exposures of the Islamic Bank calculated in accordance with sub-rules (3) to (6) of this rule.

(3) The Exposure Measure referred in Rule 5.7 (2) (b) must be calculated as the sum of:

(a) on-balance sheet items; and

(b) off-balance sheet items.

(4) In relation to on-balance sheet items:

(a) for securities financing transactions, the exposure value must be calculated in accordance with IFRS and the netting requirements referred in Rules on Credit Risk Mitigation (CRM) in Chapter 6 of IBB Module;

(b) for Derivatives, including financing protection sold, the exposure value must be calculated as the sum of the on-balance sheet value in accordance with IFRS and an add-on for potential future exposure calculated in accordance with Rules on Credit Risk Mitigation in Chapter 6 of IBB Module; and

(c) for other on-balance sheet items, the exposure value must be calculated based on their balance sheet values in accordance with Rules in Chapter 6 of IBB Module.

(5) In relation to off-balance sheet items:

(a) for commitments that are unconditionally cancellable at any time by the Islamic Bank without prior notice, the exposure value should be the notional amount for the item multiplied by a Credit Conversion Factor of 10%; and

(b) for other off-balance sheet items, including:

(і) direct financing substitutes;

(ii) certain transaction-related contingent items;

(iii) short-term self-liquidating trade-related contingent items and commitments to underwrite debt and equity securities;

(iv) note issuance facilities and revolving underwriting facilities;

(v) transactions, other than SFTs, involving the posting of securities held by the Islamic Bank as collateral;

(vi) asset sales with recourse, where the financing risk remains with the Islamic Bank;

(vii) other commitments with certain drawdown;

(viii) any other commitments; and

(ix) unsettled transactions.

the exposure value must be calculated as the notional amount for each of the items multiplied by a Credit Conversion Factor of 100%.

(6) For the purpose of determining the Exposure Measure, the value of exposures of an Islamic Bank must be calculated in accordance with the International Financial Reporting Standards (IFRS) subject to the following adjustments:

(a) on-balance sheet, non-derivative exposures must be net of specific allowances and valuation adjustments (e.g. financing valuation adjustments);

(b) physical or financial collateral, guarantees or Credit Risk Mitigation purchased must not be used to reduce on-balance sheet exposures; and

(c) financings or other exposures must not be netted with PSIA/deposits or investments made collateralizing them.

6. CREDIT RISK

6.1. General

(1) This Chapter sets out the requirements for an Islamic bank’s Credit Risk management policy (including Credit Risk assessments and the use of ratings from ECRAs):

(a) to implement the risk-based framework for capital adequacy; and

(b) to ensure the early identification and management of problem assets.

(2) This Chapter also deals with the following means to determine Regulatory Capital and control or mitigate Credit Risk:

(a) the Risk-Weighted Assets approach;

(b) CRM techniques;

(c) provisioning.

(3) To guard against abuses and to address conflicts of interest, this Chapter requires transactions with related parties to be at arm’s length.

6.2. Credit Risk

Credit Risk is:

(a) the risk of default by counterparties; and

(b) the risk that an asset will lose value because its credit quality has deteriorated.

Guidance

Credit Risk may result from on-balance-sheet and off-balance-sheet exposures, including financing and advances, investments, inter-bank financing, securities financing transactions and trading activities. It can exist in a firm’s Trading Book or Banking Book.

Examples of sources of Credit Risks in Islamic Bank

(і) accounts receivable in murabahah contracts;

(ii) counterparty risk in salam contracts;

(iii) accounts receivable and counterparty risk in istisna contracts;

(iv) lease payments receivable in ijarah contracts;

(v) sukuk held in the Banking Book;

(vi) capital impairment from investments, based on mudarabah or musharakah contracts, held in the Banking Book.

6.3. Requirements—management of Credit Risk and problem assets

(1) An Islamic Bank must manage Credit Risk by adopting a prudent Credit Risk management policy that allows its Credit Risk to be identified, measured, evaluated, managed and controlled or mitigated.

(2) The policy must also provide for problem assets to be recognised, measured and reported. The policy must set out the factors that must be taken into account in identifying problem assets.

(3) Problem asset includes impaired credit and other assets if there is reason to believe that the amounts due may not be collectable in full or in accordance with their terms.

6.4. Role of Governing Body—Credit Risk

An Islamic bank’s Governing Body must ensure that the Islamic Bank’s Credit Risk management policy gives an Islamic Bank a comprehensive bank-wide view of its Credit Risk and covers the full credit lifecycle (including credit underwriting, credit evaluation, and the management of the Islamic bank).

6.5. Credit Risk management policy

(1) An Islamic Bank must establish and implement a Credit Risk management policy:

(a) that is appropriate for the nature, scale and complexity of its business and for its risk profile; and

(b) that enables an Islamic Bank to identify, measure, evaluate, manage and control or mitigate Credit Risk.

(c) The objective of the policy is to give an Islamic Bank the capacity to absorb any existing and estimated future losses arising from Credit Risk.

6.6. Policies—general Credit Risk environment

An Islamic bank’s Credit Risk management policy must include:

(a) a well-documented and effectively-implemented process for assuming Credit Risk that does not rely unduly on external credit ratings;

(b) well-defined criteria for approving credit (including prudent underwriting standards), and renewing, refinancing and restructuring existing credit;

(c) a process for identifying the approving AFSA for credit, given its size and complexity;

(d) effective Credit Risk administration, including:

(і) periodic analysis of counterparties’ ability and willingness to repay; and

(ii) monitoring of documents, legal covenants, contractual requirements, and collateral and other CRM techniques;

(e) effective systems for the accurate and timely identification, measurement, evaluation, management and control or mitigation of Credit Risk, and reporting to an Islamic Bank’s Governing Body and senior management;

(f) procedures for tracking and reporting exceptions to, and deviations from, credit limits or policies;

(g) prudent and appropriate credit limits that are consistent with an Islamic Bank’s risk tolerance, risk profile and Capital; and

(h) effective controls for the quality, reliability and relevance of data and validation procedures.

Guidance

Depending on the nature, scale and complexity of an Islamic bank’s Credit Risk, and how often it provides credit or incurs Credit Risk, its Credit Risk management policy should include:

(1) how an Islamic Bank defines and measures Credit Risk;

(2) an Islamic Bank’s business aims in incurring Credit Risk, including:

(a) identifying the types and sources of Credit Risk that an Islamic Bank will permit itself to be exposed to (and the limits on that exposure) and those that it will not

(b) setting out the degree of diversification that an Islamic Bank requires, an Islamic Bank’s tolerance for risk concentrations and the limits on exposures and concentrations

(c) stating the risk-return trade-off that an Islamic Bank is seeking to achieve;

(3) the kinds of credit to be offered, and ceilings, pricing, profitability, maximum maturities and ratios for each kind of credit;

(4) a ceiling for the total credit portfolio (in terms, for example, of financing-to-deposit ratio, undrawn commitment ratio, maximum amount or percentage of an Islamic Bank’s Capital);

(5) portfolio limits for maximum gross exposures by region or country, by industry or sector, by category of counterparty (such as banks, non-bank financial entities and corporate counterparties), by product, by counterparty and by connected counterparties;

(6) limits, terms and conditions, approval and review procedures and records kept for financing to connected counterparties;

(7) types of collateral, financing-to-value ratios and criteria for accepting guarantees;

(8) the detailed limits for Credit Risk, and a Credit Risk structure, that:

(a) takes into account all significant risk factors, including intra-group exposures

(b) is commensurate with the scale and complexity of an Islamic Bank’s activities

(c) is consistent with an Islamic Bank’s business aims, historical performance, and the amount of capital it is willing to risk;

(9) procedures for:

(a) approving new products and activities that give rise to Credit Risk

(b) regular risk position and performance reporting;

(c) approving and reporting exceptions to limits;

(10) allocating responsibilities for implementing the Credit Risk management policy and monitoring adherence to, and the effectiveness of, the policy; and

(11) the required information systems, staff and other resources.

6.7. Credit Risk Management Policy

(1) An Islamic bank’s Credit Risk management policy must require that financing decisions are free of conflicts of interest and are made on an arm’s-length basis. In particular, the financing approval and review functions must be independent of the financing initiation function.

(2) An Islamic bank’s Credit Risk management policy must provide for monitoring the total indebtedness of each counterparty and any risk factors that might result in default (including any significant unhedged foreign exchange risk).

(3) The policy must include stress-testing an Islamic Bank’s financing exposures at intervals appropriate for the nature, scale and complexity of an Islamic Bank’s business and for its risk profile. It must also include a yearly review of stress scenarios, and procedures to make any necessary changes arising from the review.

(4) The policy must state that decisions relating to the following are made at the appropriate level of the Islamic Bank’s senior management or Governing Body:

(a) exposures exceeding a stated amount or percentage of an Islamic Bank’s capital;

(b) exposures that, in accordance with criteria set out in the policy, are especially risky;

(c) exposures that are outside an Islamic Bank’s core business.

(5) An Islamic Bank must give the AFSA full access to information in its financing portfolio, including access to staff involved in assuming, managing and reporting on Credit Risk.

Guidance

(1) This rule excludes arrangements such as an employee financing scheme, so long as the policy ensures that the scheme’s terms, conditions and limits are generally available to employees and adequately addresses the risks and conflicts that arise from financing under it.

(2) The Credit Risk management policy of an Islamic Bank should clearly set out who has the authority to approve financing to employees.

(3) The authority of a credit committee or credit officer should be appropriate for the products or portfolio and should be commensurate with the committee’s or officer’s credit experience and expertise.

(4) Each approving authority should be reviewed regularly to ensure that it remains appropriate for current market conditions and the committee’s or officer’s performance.

(5) An Islamic bank’s remuneration policy should be consistent with its Credit Risk management policy and should not encourage officers to attempt to generate short-term profits by taking an unacceptably high level of risk.

(6) The level at which financing decisions are made should vary depending on the kind and amount of credit and the nature, scale and complexity of an Islamic Bank’s business. For some firms, a credit committee with formal terms of reference might be appropriate; for others, individuals with pre-assigned limits would do.

(7) An Islamic Bank should ensure, through periodic independent audits, which the financing approval function is properly managed and that financing exposures comply with prudential standards and internal limits. The results of audits should be reported directly to the Governing Body, credit committee or senior management, as appropriate.

6.8. Credit Risk assessment

Guidance

i) This section of IBB Module sets out a standardised approach for Credit Risk assessment, and requires an Islamic Bank to establish and implement policies to identify, measure, evaluate, manage and control or mitigate Credit Risk and to calculate its Credit Risk Capital Requirement.

ii) Credit Risk assessment under this Chapter is different from the evaluation (often called credit assessment) made by a firm as part of its financing approval process.

iii) Credit assessment is part of an Islamic Bank’s internal commercial decision-making for approving or refusing credit; it consists of the evaluation of a prospective counterparty’s repayment ability. In contrast, Credit Risk assessment is done by an Islamic Bank (using ratings and risk-weights set out in these rules) as part of calculating its Credit Risk Capital Requirement.