Appendix A

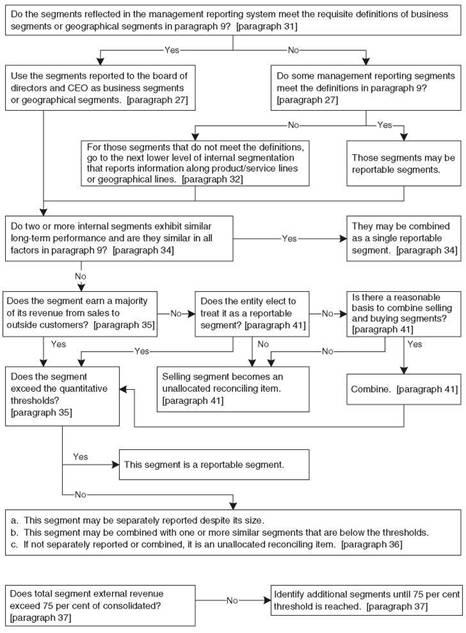

Segment definition decision tree

This appendix accompanies, but is not part of, IAS 14. Its purpose is to illustrate the application of paragraphs 27-43.

Appendix B

Illustrative segment disclosures

This appendix accompanies, but is not part of, IAS 14.

The schedule and related note presented in this appendix illustrate the segment disclosures that this Standard would require for a diversified multinational business entity. This example is intentionally complex to illustrate most of the provisions of this Standard. For illustrative purposes, the example presents comparative data for two years. Segment data is required for each year for which a complete set of financial statements is presented.

| Schedule A Information about business segments (Note 4) (All amounts million) |

| | Paper products | Office products | Publishing | Other operations | Elimination | Consolidation |

| | 20X2 | 20X1 | 20X2 | 20X1 | 20X2 | 20X1 | 20X2 | 20X1 | 20X2 | 20X1 | 20X2 | 20X1 |

| Revenue External Sales | 55 | 50 | 20 | 17 | 19 | 16 | 7 | 7 | | | | |

| Inter-segment sales | 15 | 10 | 10 | 14 | 2 | 4 | 2 | 2 | (29) | (30) | | |

| Total Revenue | 70 | 60 | 30 | 31 | 21 | 20 | 9 | 9 | (29) | (30) | 101 | 90 |

| Result | | | | | | | | | | | | |

| Segment result | 20 | 17 | 9 | 7 | 2 | 1 | 0 | 0 | (1) | (1) | 30 | 24 |

| Unallocated corporate expenses | | | | | | | | | | | (7) | (9) |

| Operating profit | | | | | | | | | | | 23 | 15 |

| Interest expense | | | | | | | | | | | (4) | (4) |

| Interest income | | | | | | | | | | | 2 | 3 |

| Share of profits of associates | 6 | 5 | | | | | 2 | 2 | | | 8 | 7 |

| Income taxes | | | | | | | | | | | (7) | (4) |

| Profit | | | | | | | | | | | 22 | 17 |

| Other Information | | | | | | | | | | | | |

| Segment Assets | 54 | 50 | 34 | 30 | 10 | 10 | 10 | 9 | | | 108 | 99 |

| Investment in equity method associates | 20 | 16 | | | | | 12 | 10 | | | 32 | 26 |

| Unallocated corporate assets | | | | | | | | | | | 35 | 30 |

| Consolidated total assets | | | | | | | | | | | 175 | 155 |

| Segment liabilities | 25 | 15 | 8 | 11 | 8 | 8 | 1 | 1 | | | 42 | 35 |

| Unallocated corporate liabilities | | | | | | | | | | | 40 | 55 |

| Consolidated total liabilities | | | | | | | | | | | 82 | 90 |

| Capital expenditure | 12 | 10 | 3 | 5 | 5 | | 4 | 3 | | | | |

| Depreciation | 9 | 7 | 9 | 7 | 5 | 3 | 3 | 4 | | | | |

| Non-cash expenses other than depreciation | 8 | 2 | 7 | 3 | 2 | 2 | 2 | 1 | | | | |

Note 4 Business and geographical segments (all amounts million)

Business segments: for management purposes, the Company is organised on a worldwide basis into three major operating divisions - paper products, office products and publishing - each headed by a senior vice-president. The divisions are the basis on which the Company reports its primary segment information. The paper products segment produces a broad range of writing and publishing papers and newsprint. The office products segment manufactures labels, binders, pens, and markers and also distributes office products made by others. The publishing segment develops and sells loose-leaf services, bound volumes and CD-ROM products in the fields of taxation, law and accounting. Other operations include development of computer software for specialised business applications for unaffiliated customers and development of certain former productive timberlands into vacation home sites. Financial information about business segments is presented in Schedule A.

Geographical segments: although the Company's three divisions are managed on a worldwide basis, they operate in four principal geographical areas of the world. In the United Kingdom, its home country, the Company produces and sells a broad range of papers and office products. Additionally, all of the Company's publishing and computer software development operations are conducted in the United Kingdom, though the published loose-leaf and bound volumes and CD-ROM products are sold throughout the United Kingdom and Western Europe. In the European Union, the Company operates paper and office products manufacturing facilities and sales offices in the following countries: France, Belgium, Germany and the Netherlands. Operations in Canada and the United States are essentially similar and consist of manufacturing papers and newsprint that are sold entirely within those two countries. Most of the paper pulp comes from Company-owned timberlands in the two countries. Operations in Indonesia include the production of paper pulp and the manufacture of writing and publishing papers and office products, almost all of which is sold outside Indonesia, both to other segments of the Company and to external customers.

Sales by market: the following table shows the distribution of the Company's consolidated sales by geographical market, regardless of where the goods were produced:

| | Sales revenue by geographical market |

| | 20X2 | 20X1 |

| United Kingdom | 19 | 22 |

| Other European Union countries | 30 | 31 |

| Canada and the United States | 28 | 21 |

| Mexico and South America | 6 | 2 |

| Southeast Asia (principally Japan and Taiwan) | 18 | 14 |

| | 101 | 90 |

Assets and additions to property, plant, equipment, and intangible assets by geographical area: the following tables show the carrying amount of segment assets and additions to property, plant, equipment, and intangible assets by geographical area in which the assets are located:

| | Carrying amount of segment assets | Additions to property, plant, equipment, and intangible assets |

| | 20X2 | 20X1 | 20X2 | 20X1 |

| United Kingdom | 72 | 78 | 8 | 5 |

| Other European Union countries | 47 | 37 | 5 | 4 |

| Canada and the United States | 34 | 20 | 4 | 3 |

| Indonesia | 22 | 20 | 7 | 6 |

| | 175 | 155 | 24 | 18 |

Segment revenue and expense: in Belgium, paper and office products are manufactured in combined facilities and are sold by a combined sales force. Joint revenues and expenses are allocated to the two business segments. All other segment revenue and expense is directly attributable to the segments.

Segment assets and liabilities: segment assets include all operating assets used by a segment and consist principally of operating cash, receivables, inventories and property, plant and equipment, net of allowances and provisions. While most such assets can be directly attributed to individual segments, the carrying amount of certain assets used jointly by two or more segments is allocated to the segments on a reasonable basis. Segment liabilities include all operating liabilities and consist principally of accounts, wages, and taxes currently payable and accrued liabilities. Segment assets and liabilities do not include deferred income taxes.

Inter-segment transfers: segment revenue, segment expenses and segment result include transfers between business segments and between geographical segments. Such transfers are accounted for at competitive market prices charged to unaffiliated customers for similar goods. Those transfers are eliminated in consolidation.

Unusual item: sales of office products to external customers in 20X2 were adversely affected by a lengthy strike of transportation workers in the United Kingdom, which interrupted product shipments for approximately four months. The Company estimates that sales of office products were approximately half of what they would otherwise have been during the four-month period.

Investment in equity method associates: the Company owns 40 per cent of the capital stock of EuroPaper Ltd, a specialist paper manufacturer with operations principally in Spain and the United Kingdom. The investment is accounted for by the equity method. Although the investment and the Company's share of EuroPaper's net profit are excluded from segment assets and segment revenue, they are shown separately in conjunction with data for the paper products segment. The Company also owns several small equity method investments in Canada and the United States whose operations are dissimilar to any of the three business segments.

Appendix C

Summary of required disclosure

This appendix accompanies, but is not part of, IAS 14. Its purpose is to summarise the disclosures required by paragraphs 49-83 for each of the three possible primary segment reporting formats.

[¶хх] refers to paragraph xx in the Standard.

| Primary format is business segments | Primary format is geographical segments by location of assets | Primary format is geographical segments by location of customers |

| Required primary disclosures: | Required primary disclosures: | Required primary disclosures: |

| Revenue from external customers by business segment [¶51] | Revenue from external customers by location of assets [¶51] | Revenue from external customers by location of customers [¶51] |

| Revenue from transactions with other segments by business segment [¶51] | Revenue from transactions with other segments by location of assets [¶51] | Revenue from transactions with other segments by location of customers [¶51] |

| Segment result by business segment [¶52] | Segment result by location of assets [¶52] | Segment result by location of customers [¶52] |

| Carrying amount of segment assets by business segment [¶55] | Carrying amount of segment assets by location of assets [¶55] | Carrying amount of segment assets by location of customers [¶55] |

| Segment liabilities by business segment [¶56] | Segment liabilities by location of assets [¶56] | Segment liabilities by location of customers [¶56] |

| Cost to acquire property, plant, equipment, and intangibles by business segment [¶57] | Cost to acquire property, plant, equipment, and intangibles by location of assets [¶57] | Cost to acquire property, plant, equipment, and intangibles by location of customers [¶57] |

| Depreciation and amortisation expense by business segment [¶58] | Depreciation and amortisation expense by location of assets [¶58] | Depreciation and amortisation expense by location of customers [¶58] |

| Non-cash expenses other than depreciation and amortisation by business segment [¶61] | Non-cash expenses other than depreciation and amortisation by location of assets [¶61] | Non-cash expenses other than depreciation and amortisation by location of customers [¶61] |

| Share of profit or loss of [¶64] and investment in [¶66] equity method associates or joint ventures by business segment (if substantially all within a single business segment) | Share of profit or loss of [¶64] and investment in [¶66] equity method associates or joint ventures by location of assets (if substantially all within a single segment) | Share of profit or loss of [¶64] and investment in [¶66] equity method associates or joint ventures by location of customers (if substantially all within a single segment) |

| Reconciliation of revenue, result, assets, and liabilities by business segment [¶67] | Reconciliation of revenue, result, assets, and liabilities [¶67] | Reconciliation of revenue, result, assets, and liabilities [¶67] |

| Primary format is business segments | Primary format is geographical segments by location of assets | Primary format is geographical segments by location of customers |

| Required secondary disclosures: | Required secondary disclosures: | Required secondary disclosures: |

| Revenue from external customers by location of customers [¶69] | Revenue from external customers by business segment [¶70] | Revenue from external customers by business segment [¶70] |

| Carrying amount of segment assets by location of assets [¶69] | Carrying amount of segment assets by business segment [¶70] | Carrying amount of segment assets by business segment [¶70] |

| Cost to acquire property, plant, equipment, and intangibles by location of assets [¶69] | Cost to acquire property, plant, equipment, and intangibles by business segment [¶70] | Cost to acquire property, plant, equipment, and intangibles by business segment [¶70] |

| - | Revenue from external customers by geographical customers if different from location of assets [¶71] | - |

| - | - | Carrying amount of segment assets by location of assets if different from location of customers [¶72] |

| - | - | Cost to acquire property, plant, equipment, and intangibles by location of assets if different from location of customers [¶72] |

| Primary format is business segments | Primary format is geographical segments by location of assets | Primary format is geographical segments by location of customers |

| Other required disclosures: | Other required disclosures: | Other required disclosures: |

| Revenue for any business or geographical segment whose external revenue is more than 10 per cent of entity revenue but that is not a reportable segment because a majority of its revenue is from internal transfers [¶74] | Revenue for any business or geographical segment whose external revenue is more than 10 per cent of entity revenue but that is not a reportable segment because a majority of its revenue is from internal transfers [¶74] | Revenue for any business or geographical segment whose external revenue is more than 10 per cent of entity revenue but that is not a reportable segment because a majority of its revenue is from internal transfers [¶74] |

| Basis of pricing inter-segment transfers and any change therein [¶75] | Basis of pricing inter-segment transfers and any change therein [¶75] | Basis of pricing inter-segment transfers and any change therein [¶75] |

| Changes in segment accounting policies [¶76] | Changes in segment accounting policies [¶76] | Changes in segment accounting policies [¶76] |

| Types of products and services in each business segment [¶81] | Types of products and services in each business segment [¶81] | Types of products and services in each business segment [¶81] |

| Composition of each geographical segment [¶81] | Composition of each geographical segment [¶81] | Composition of each geographical segment [¶81] |